Navigating Distressed Business Finance.

Strategic Solutions and Ethical Approaches.

Ethical Distressed Finance: A Strategic Imperative.

The contemporary economic environment presents significant challenges for small and medium-sized businesses, frequently pushing them into financial distress.

A notable driver of this hardship is the Australian Tax Office's (ATO) increasingly aggressive stance on debt enforcement, coupled with the unexpected resurgence of legacy debts, often demanding immediate repayment within tight deadlines.

Traditional financing avenues frequently prove insufficient or inaccessible in these high-pressure scenarios, leaving businesses vulnerable.

The Changing Environment.

The ATO has adopted a more aggressive approach to debt enforcement, and many businesses are being unexpectedly confronted with old debts, creating immediate, high-stakes crises. Traditional financing often falls short in these situations.

Beyond Interest Rates.

The value of distressed finance goes beyond just interest rates. Our firm emphasises that factors like speed, flexibility, and a clear long-term strategy for recovery are equally important. Businesses are increasingly using the equity in their property as a more effective and less risky way to secure funding.

FoS's Holistic Approach to Distressed Finance.

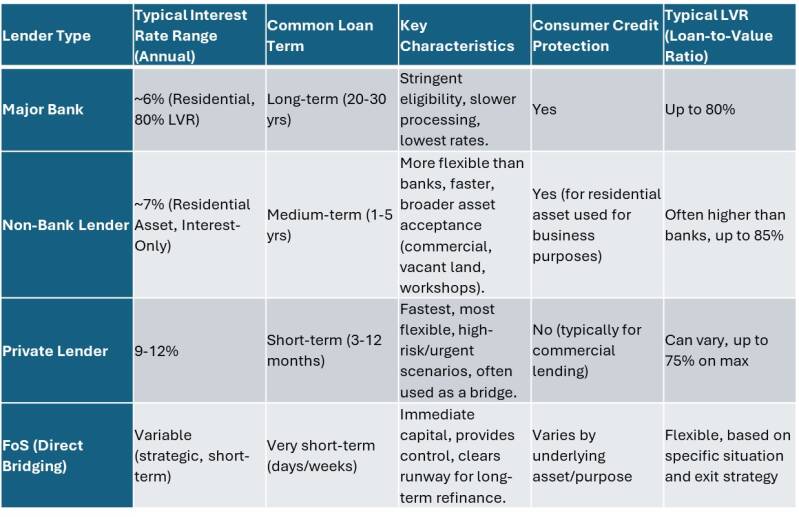

The FoS Group, operates with a distinctive business model, Our comprehensive approach encompasses engagement with the full spectrum of lending institutions: traditional banks, non-bank lenders, and the private market. This extensive reach enables us to customise financial solutions to meet the diverse and often complex needs of our clientele.

Our company operates as both a broker of lending and Business advisory that can provide crucial bridging finance to quickly pay off urgent creditors and create time for a more sustainable, long-term refinancing plan and Business Turnaround.

Strategic Interventions.

Many businesses are facing aggressive creditors. We at FoS can facilitate short-term loans to clear immediate debts and provide for working capital needs, enabling your business to successfully refinance with a more sustainable lender.

Supporting Business Restructuring:

FoS plays a significant role in helping businesses undergoing Small Business Restructuring (SBR), a formal process that can often make businesses unlendable by traditional banks. FoS's willingness to facilitate loans in these complex situations is critical for the success of many restructuring plans.

Dispelling Misconceptions:

While short-term distressed finance has a high annualized cost, its strategic use over a brief period makes it a valuable and often cost-effective solution for businesses in crisis, especially when it prevents a collapse or enables a long-term recovery.

Current Triggers for Business Distress.

The financial health of numerous businesses has been significantly impacted by recent shifts in regulatory enforcement and the surfacing of long-standing liabilities.

A prominent and recent cause of current financial hardship is the Australian Tax Office (ATO) adopting a "more aggressive approach to debt enforcement over the last 12 months". This renewed focus has directly compelled many businesses into the "arms of the insolvency industry" as they seek viable solutions to their burgeoning problems.

Another pervasive issue is where businesses are unexpectedly confronted with demands for payment, often with extremely short deadlines, such as "all due in 21 days". This phenomenon points to a backlog of unaddressed or deferred financial obligations now being actively pursued, these latent debts are a systemic issue of unmanaged liabilities within most of the small business sectors.

This is not merely about new financial difficulties but the surfacing of historical issues, potentially exacerbated by broader economic pressures or changes in enforcement policies. This implies that many businesses might be unknowingly sitting on similar financial vulnerabilities, making the need for proactive financial health checks and our strategic advisory more urgent than ever.

The causal relationship here is that past financial mismanagement or deferral, combined with current enforcement trends, creates immediate, high-stakes crises that demand swift and decisive action.

The Shift Towards Flexible Lending and Leveraging Property Equity.

In response to these pressures, we see that businesses are increasingly gravitating towards our flexible lenders that give them better terms. "Better terms" now encompasses flexibility, strategic alignment, and a clear pathway to recovery, not solely the lowest interest percentage point.

There is a growing recognition that the "longer-term process" and the overarching "strategy" are as crucial as the interest rate itself. This signifies a growing sophistication in borrower understanding, where the prioritisation of holistic value supersedes simple cost. We believe "it's not just about the interest rate, it's about the longer-term process and the Turnaround strategy that now reveals a deeper understanding amongst our distressed borrowers. This suggests a market where the comprehensive solution and its strategic impact are highly valued, leading to a more sophisticated and client-centric distressed finance market.

Furthermore, there is a growing realisation that the "equity in their property" can be utilised "far more effectively" and with "less risk to their personal assets than using traditional business type financing". This highlights our strategic pivot towards asset-backed solutions, potentially offering a safer alternative compared to the often unregulated and aggressive nature of some unsecured business loans. This evolving preference underscores our strategic adaptation by businesses seeking more secure and manageable financial pathways in challenging times.

The Unique Role of Direct Lending and Bridging Finance.

A significant differentiator for FoS is our direct lending capability, which is specifically deployed when people are in really bad situations with creditors that are getting upset and they need a quick outcome.

This direct lending capacity allows us to facilitate crucial "bridging finance" to "clear the runway" for a defined period. This immediate intervention enables the swift payout of urgent creditors and provides essential time to prepare for a more conventional, long-term refinance and Business Turnaround.

This approach was powerfully demonstrated in the case of "James".

James , a seller of tractors and light machinery, faced a spiraling, very expensive" business loan from an "unregulated" lender who offered no mercy on defaults. James owed $220,000 to this lender and needed an additional $30,000 for critical purchase orders, he anticipated also a $15,000 ATO debt.

His home, valued at $420,000, represented a significant equity source.

FoS immediately engaged the aggressive lender, securing a 7-day payout letter. Critically, FoS then directly lent James the necessary capital (approximately $220-230k) to pay out the urgent business lender and provide vital working capital for his purchase orders.

Our direct intervention created a reprieve and the grace of time before a formal refinance. The element of control is a critical, yet often overlooked benefit in highly distressed situations. Our services also encompasses the managing of aggressive creditors, ensuring strict deadlines are met, and meticulously guiding the client through complex refinance processes without the risk of further defaults.

This suggests that for businesses in acute distress, our expert management of the crisis by an experienced financial partner is as valuable, if not more so, than the capital itself, preventing a further spiral into unrecoverable debt.

Subsequently FoS managed the refinance process to a more sustainable non-bank lender, leveraging James 's residential property as security.

This strategic direct intervention proved critical in a scenario where the original lender offered "no mercy" on defaults, ultimately being "far far less expensive for him doing it that way" than alternative distressed finance options.

Collaboration with Insolvency Practitioners, Particularly in Small Business Restructuring (SBR).

A massive part of FoS's business involves working with companies entering or already under Small Business Restructuring (SBR). We possess a deep understanding that an SBR appointment immediately raises red flags for most traditional lenders, creating a significant hurdle for businesses seeking finance during restructuring.

The fact that a formal restructuring mechanism designed to save businesses simultaneously renders them unlendable by conventional means creates a significant paradox.

FoS's willingness and ability to lend into or around SBRs effectively mitigates this "red flag" for our clients.

Our Group has a sophisticated understanding of the SBR process and a willingness to assess underlying business viability rather than simply relying on a credit score that reflects formal administration. Our specialised lenders are crucial enablers of formal restructuring processes, without whom many SBRs might fail due to lack of funding.

FoS's expertise lies in providing the necessary capital during SBRs, recognising that proposals (e.g., a 75 cents in the dollar payout) often require immediate funds (e.g., the remaining 25 cents) which are frequently tied up in illiquid assets like property equity. Our willingness to lend in these complex situations stems from our conviction that businesses undertaking SBR fully intend to actually continue to trade, viewing it as a strategic investment in viable enterprises.

This was evident in another of our cases. namely a furniture transport removals company, where FoS successfully brokered a non-bank loan to fund the SBR proposal, enabling the business to meet its obligations and continue operating. This case scenario explicitly proves that while the SBR practitioner had initiated negotiations, capital was critically needed to "settle and meet the requirements" of the proposal. This demonstrates that formal insolvency processes, while providing a legal and structural framework for recovery, often require external financial injections to be successful and effective.

FoS's role here is not just that of a lender but a crucial enabler of the SBR process itself. and a critical partnership between insolvency experts and specialised finance providers, forming a collaborative ecosystem essential for successful business rehabilitation.

Demystifying Distressed Finance: Costs and Structures.

A common misconception surrounding distressed finance involves perceptions of "raptor style lending or predatory lending practices". While acknowledging that unfortunately there's a bit of a stain from people that are not acting in ways which are good within the industry, FoS strongly emphasizes its commitment to doing things correctly with the intention of helping people long-term.

The common perception of high-cost, predatory lending is often based on a misunderstanding of how short-term finance is strategically applied.

While short-term finance is indeed far more expensive than what you would get at a bank on an annualised basis, its actual cost is significantly mitigated if used for a very brief, strategic period (e.g., "45 days while you prepare your application to go back to a second tier or a sub major bank").

This strategic application fundamentally alters the cost-benefit analysis.

Comparative Lending Rates and Terms for Distressed Finance

Detailed Comparison of Interest Rates and Terms.

The market perception of distressed lending rates (e.g., "2 and 3% per month") is largely inaccurate; the market has moved a lot in recent years due to increased competition and a better understanding of the complex circumstances faced by distressed businesses.

It is crucial to understand that a 9-12% annual rate for private lending, if utilised for only a short duration (e.g., "3 months"), does not incur the full annual differential. The cost is strictly pro-rated for the actual usage period, making it significantly less expensive than the perceived annual rate might suggest for short-term, strategic use. This re-framing of cost from a misleading annual perspective to a more accurate, transactional, and time-bound one is vital to properly assess the commercial viability of such short-term solutions, as misinterpreting the annual rate can lead to rejecting a potentially life-saving option.

The Impact of Urgency and Asset Type on Financing Costs.

"Urgency is everything" when it comes to distressed lending. If a solution "needs to be done in 24 hours, it's going to be more expensive". which is the premium placed on speed and immediate liquidity in crisis situations.

Our statements "urgency is everything" and "the longer you wait the more expensive it's going to get" establish a clear inverse relationship as the need for speed increases, so does the cost of finance, and as time to act decreases, your options narrow.

This is a fundamental principle of distressed finance, implying that the value of rapid access to capital in a crisis often outweighs its higher nominal interest rate, especially if it is a temporary bridge. This causal relationship underscores the critical importance of early intervention and proactive planning to secure more favorable terms.

The type of asset used as security (e.g., residential property, vacant land, commercial properties like workshops, or even highly niche assets like moorings and houseboats) significantly influences our available lenders, their risk appetite, and the associated rates. Our Non-bank lenders can often accommodate a broader range of commercial assets than major banks before it becomes necessary to resort to more expensive private lending.

The Critical Importance of Early Engagement and Intervention.

Strategic Considerations for Businesses and Advisors, A consistent and paramount theme throughout the discussion is that "the longer you wait the more expensive it's going to get". Early engagement provides access to "more options" and allows for solutions closer to "bank rates", significantly reducing the overall cost and complexity. This proactive approach can lead to "cheaper," "quicker," and "easier" resolutions, ultimately enabling businesses to "trade onwards" rather than facing liquidation.

This highlights the "time-cost" continuum in distressed finance, where the value of rapid access to capital in a crisis often outweighs its higher nominal interest rate, especially if it is a temporary bridge. This causal relationship underscores the critical importance of early intervention and proactive planning to secure more favourable terms.

Early Engagement: The Smart Move in Distressed Finance.

Delaying action in times of financial stress can be costly. Early engagement unlocks more funding options, often at rates closer to traditional bank lending. It leads to faster, simpler resolutions and helps businesses stay operational. Acting early isn’t just strategic it’s essential to preserving value and avoiding liquidation.

Why Early Engagement Matters: And How It Saves You More Than Money.

When financial pressure builds, waiting can be the most expensive decision. Early engagement gives you access to more options, better rates, and faster resolutions. It’s not just about cost it’s about control. By acting early, you can avoid liquidation, preserve business continuity, and secure terms that work in your favour.

Evaluating Commercial Sense: When to Pursue Restructuring versus Considering Alternative Paths.

FoS operates on the fundamental principle that "just because you can take a loan and pay out one debt doesn't necessarily mean that you should. Our role extends beyond merely facilitating funds to comprehensively assessing the "overall picture" and diagnosing whether a financial solution truly makes commercial sense for our client's long-term viability.

This involves an honest and often difficult appraisal of whether it is sometimes better to draw a line in the sand and let some of these things go rather than commit into an unfruitful or unsuccessful attempt to rehabilitate a Business.

This is acknowledged as a really hard decision for people to make, highlighting the profound emotional aspect of business distress and the need for objective, empathetic advice. The repeated emphasis on assessing "commercial sense" and the explicit willingness to advise against a loan, even when one is possible, positions FoS not merely as a facilitator of funds, but as an ethical gatekeeper. In situations of desperation because businesses might be inclined to take on unsustainable debt, further exacerbating their problems.

Our services are also to provide objective, long-term viability assessment, even if it means recommending the difficult path of liquidation. This is the true value of our distressed finance expertise which lies in our judgment and integrity, protecting clients from throwing good money after bad.

The Value of Transparency and Acting in the Client's Best Interest.

Our role transcends more than being facilitators of loan arrangements, we are a sophisticated strategic financial partner, a crisis manager, and a highly ethical advisory providing comprehensive, value-added services that addresses the intricate needs of distressed businesses and solvent businesses alike whereto survive or expand.

The value provided by the FoS group extends significantly beyond merely providing capital. We provide a crucial strategic advisory, transparent cost structures and an ethical approach that consistently prioritises the client's commercial viability, even if it means advising against a loan or advise to enter into formal insolvency.

We rely upon a synergistic network of trusted professionals working together seamlessly to provide "holistic solutions".

We work in close collaboration with Insolvency practitioners, accountants, specialised finance brokers that all help you successfully navigate your business distress thus relieving you of taking on the burden singularly.

Move quickly and strategically to protect your business.

We encourage businesses facing distress to actively seek out and leverage our integrated advisory ecosystem, as a multi-disciplinary approach significantly enhances the chances of successful survival, recovery, and long-term viability.

The future of business support in challenging economic times will increasingly rely on such holistic, client-centric partnerships that can offer both tailored financial solutions and sound strategic guidance, fostering resilience and long-term sustainability for small and medium-sized enterprises.